Canfor Reports Results for Second Quarter of 2020

Canfor Corporation (“The Company” or “Canfor”) reported its second quarter 2020 results:

Overview

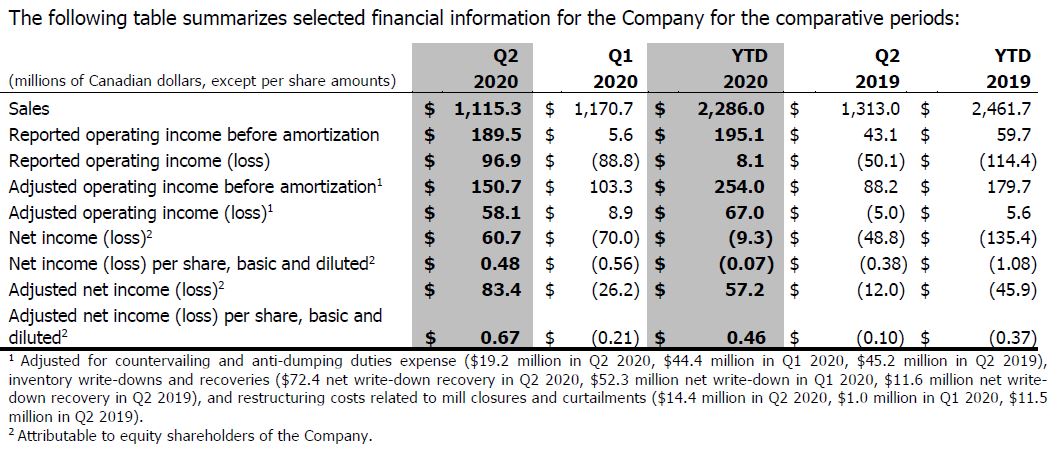

– Second quarter of 2020 reported operating income of $97 million, includes $81 million recovery of previous inventory write-downs in the lumber segment

– Adjusted shareholder net income of $83 million, or $0.67 per share

– Vida Group (“Vida”) announced agreement to purchase Bergs Timber Production AB (“Bergs”) sawmill assets for $43 million plus working capital, which will add 215 million board feet to Vida’s annual capacity

– Completed acquisition of Elliott Sawmilling Co., LLC (“Elliott”)

– Announced permanent closure of Isle Pierre sawmill, located near Prince George, British Columbia (“BC”) due to an insufficient supply of economically viable timber

Financial Results

For the second quarter of 2020, the Company reported operating income of $96.9 million, $185.7 million higher than the operating loss of $88.8 million reported for the first quarter of 2020, reflecting materially higher earnings in the lumber segment, offset in part by a moderate decline in pulp and paper segment earnings.

Results in the second quarter of 2020 included an $80.6 million recovery in the lumber and log inventory write-down provisions, partly offset by an $8.2 million inventory write-down for the pulp and paper segment, as well as a countervailing (“CVD”) and anti-dumping duties (“ADD”) expense of $19.2 million and restructuring costs of $14.4 million, largely related to the announced permanent closure of the Company’s Isle Pierre sawmill (which will take effect in the third quarter following an orderly wind down of operations). After adjusting for the aforementioned items, the Company’s operating income was $58.1 million for the second quarter of 2020, up $49.2 million from similarly adjusted operating income of $8.9 million in the first quarter of 2020.

Despite the significant disruptive impacts of the coronavirus outbreak (“COVID-19”) across the Canfor organization, adjusted lumber segment operating results compared favourably with the previous quarter, reflecting significantly improved market conditions and earnings from the Company’s Southern Yellow Pine (“SYP”) and European Spruce/Pine/Fir (“SPF”) operations, as well as a more modest improvement in its Western SPF operating results.

As a result of a significant reduction in demand due to COVID-19 in April, the Company’s Western SPF region took extensive production curtailments in April and May. Following a return to more normal operating rates in June, along with improved US-dollar prices and a 3% weaker Canadian dollar, the region had much improved operating results towards the end of the quarter. The Company’s US South region also experienced downtime early in the quarter as a result of the pandemic, but benefited from significant SYP price gains during May and June, as a sharp pick-up in demand outpaced available supply, and this, in combination with strong operating rates, contributed to a solid financial performance in the current quarter. The Company’s European SPF operational results also saw a marked improvement in the latter part of the quarter, more than offsetting the impact of COVID-19 related curtailments earlier in the period.

Reflecting the pronounced effects from COVID-19, US housing starts fell dramatically in April, dropping to their lowest levels since early 2015 (averaging 934,000 units). Through May and June, lumber markets rebounded, with both repair and remodeling and new home construction activity seeing a strong uptick. Against a backdrop of lean supply chain inventories, the unexpected increase in demand resulted in a spike in prices, starting in May for most SYP dimensions followed by Western SPF in June. June housing starts averaged 1,186,000 units, and, for the second quarter of 2020, on a seasonally adjusted basis, averaged 1,044,000 units, down 30% from the previous quarter, largely due to the aforementioned drop early in the current quarter. In Canada, home construction and repair and remodeling activity was more muted; housing starts averaged 191,000 units on a seasonally adjusted basis in the second quarter of 2020, down 9% from the previous quarter, largely reflecting slowing activity in all major Canadian cities.

Offshore demand for Western SPF products improved slightly through the second quarter as trade barriers enacted at the onset of COVID-19 were slowly lifted and the impacts of the virus lessened. Towards the end of the quarter, however, both domestic and export demand in China declined. In Japan and Korea, markets improved modestly quarter-over-quarter, but softened near the end of the quarter. Western European and Scandinavian lumber demand was strong through the latter part of the second quarter, driven largely by the strength in the repair and remodeling sector.

Despite the sharp decline in the benchmark North American Random Lengths Western SPF 2×4 #2&Btr price in April to a low of US$282 per Mfbm, prices inched steadily upwards in May before climbing considerably in June, ending the quarter at US$432 per Mfbm. The Company’s Western SPF lumber unit sales realizations remained relatively flat quarter-over-quarter, as favourable offshore unit sales realizations, decreased CVD and ADD expenses and a weaker Canadian dollar in the current quarter substantially offset a US$42 per Mfbm, or 11%, decline in the average Western SPF 2×4 #2&Btr benchmark price to US$357 per Mfbm.

The significant increase in lumber prices towards the end of the quarter and into July, combined with improved market demand over the same period, resulted in the full reversal of the Company’s previously recorded inventory write-down provision related to the Company’s Western SPF operations of $80.6 million at the end of the second quarter of 2020.

The Company’s SYP lumber unit sales realizations were significantly higher than the prior quarter, principally reflecting a US$77 per Mfbm, or 20%, increase in the SYP East 2×4 #2 price to US$463 per Mfbm, with similarly strong price gains seen for other wider dimensions.

The Company’s European SPF unit sales realizations were modestly higher quarter-over-quarter, as a slight decline in the average European indicative SPF lumber benchmark price (an internally generated benchmark based on delivered price to the largest continental market), to SEK 3,254 per Mfbm, was more than offset by a 3% weaker Canadian dollar (compared to the Swedish Krona (“SEK”)).

Total lumber shipments, at 1.15 billion board feet, were 8% lower than the previous quarter, largely reflecting the widespread production curtailments in April and May; as demand improved during the quarter, shipments outpaced production across all of the Company’s operating regions.

Total lumber production, at 1.04 billion board feet, was 19% below the prior quarter principally reflecting COVID-19 market-related curtailments across all three of the Company’s operating regions, but most notably in the BC Interior. Western SPF production decreased 30% from the previous quarter. SYP production experienced a 12% decline quarter-over-quarter, and, European SPF production was 5% lower than the prior period.

Lumber unit manufacturing and product costs in all operating regions were broadly in line with the previous quarter, as the incremental effect of lower production volumes was offset by lower market-related log costs and reduced discretionary spending in the current quarter. In addition, the Company’s Western SPF operations were able to access the Canada Emergency Wage Subsidy established by the federal government due to meeting the criteria of a reduction in revenue. The program enabled the Company to bring its employees back to work and restart its BC sawmills by covering a portion of employee wage costs.

In the second quarter of 2020, the Company’s 70% owned Vida subsidiary entered into an agreement to purchase three sawmills from Bergs for $43.0 million plus working capital. The transaction is expected to close in the third quarter of 2020, subject to customary closing conditions. Also during the current quarter, the Company completed the second phase purchase of Elliott Sawmilling Co., LLC (“Elliott”) on May 31, 2020, bringing its ownership interest to 100%.

Results in the pulp and paper segment for the second quarter of 2020 reflected direct and indirect impacts of COVID-19 on global markets, and more specifically Canfor Pulp Products Inc.’s (“CPPI”) pulp and paper business. Global pulp prices improved during April, resulting largely from increased demand for at-home tissue coupled with supply disruptions, principally in Latin America and Australasia; however, prices came increasingly under pressure in the back half of the current quarter reflecting a sharp decline in printing and writing demand combined with more moderated tissue purchasing activity. For the second quarter as a whole, Canadian-dollar pulp unit sales realizations showed a modest increase compared to the previous quarter, boosted by slightly higher Northern Bleached Softwood Kraft (“NBSK”) prices to North America, improved prices for Bleached Chemi-Thermo Mechanical Pulp (“BCTMP”) and a weaker Canadian dollar. The effect of COVID-19 on lumber sawmill operating rates in the BC Interior, particularly in April and May, materially impacted residual fibre supply to CPPI’s Prince George (“PG”) based operations, resulting in a three-week curtailment at CPPI’s Northwood NBSK pulp mill (“Northwood”) in the current quarter, as well as increased fibre costs reflecting a higher proportion of more expensive whole log chips.

Pulp production was 260,000 tonnes for the second quarter of 2020, down 38,000 tonnes, or 13%, from the previous quarter, principally driven by decreased operating days in the current quarter due to the three-week COVID-19 related curtailment at Northwood, which reduced pulp production by 35,000 tonnes. Improved productivity at CPPI’s Taylor BCTMP mill, which set new record-high production volumes in the current quarter, largely offset operational disruptions at CPPI’s PG pulp mill in June.

Pulp shipments were down 42,000 tonnes, or 14%, from the previous quarter, mainly due to the aforementioned decrease in pulp production quarter-over-quarter, combined with a 13,000-tonne vessel slippage at the end of June into early July 2020.

Pulp unit manufacturing costs were slightly higher than the prior quarter as the effects of increased fibre costs and the impact of reduced production in the current quarter were largely offset by seasonally lower energy costs and decreased planned maintenance spending. Fibre costs were moderately higher than the previous period primarily due to a larger proportion of higher-cost whole log chips as a result of sawmill curtailments in the current quarter.

At June 30, 2020, on a consolidated basis, the Company had total net debt of $856.0 million, down $214.0 million from the end of the previous quarter, and available liquidity of $809.3 million. Available liquidity improved by $304.5 million during the current quarter reflecting significantly higher cash earnings, a seasonal unwind of log inventories in Western Canada, various cash conservation initiatives undertaken in response to COVID-19, as well as an increase in the principal amount of the Company’s revolving credit facility from $100.0 million to $200.0 million during the period. The $200.0 million revolving facility remains undrawn and has terms that are largely consistent with those of Canfor’s existing operating loan facility. This incremental liquidity, combined with cost conservation initiatives, a disciplined approach to cash management and materially reduced capital spending through the balance of 2020, will support the Company’s efforts to preserve its solid balance sheet position.

Despite the significant impacts of the pandemic through the second quarter, lumber fundamentals have proven to be resilient, with a stronger than anticipated recovery evident in pending home sales, housing starts, repair and remodel spend, as well as sustained increases in home purchase mortgage applications. Looking forward, prices are forecast to reflect continued strong demand and current low inventory levels through the third quarter of 2020.

Lumber prices to Asian-Pacific markets through the same period are expected to remain relatively unchanged. European lumber markets are projected to remain solid through the third quarter, reflecting a strong order file and steady demand in that region.

In the pulp and paper segment, recognizing the effects on fibre supply from COVID-19 related sawmill curtailments in the second quarter, on July 6, 2020, CPPI commenced a four-week curtailment of CPPI’s PG and Intercontinental Pulp mills, which will reduce CPPI’s production output in the third quarter by approximately 38,000 tonnes of NBSK pulp and 12,000 tonnes of paper.

In addition to COVID-19 related downtime, CPPI has a maintenance outage currently scheduled at its Northwood mill in September 2020, which will continue into October to complete a capital upgrade to extend the useful life of Northwood’s number five recovery boiler (“RB5”). This Northwood outage will result in 48,000 tonnes of reduced NBSK pulp production, 30,000 tonnes of which is currently forecast for the third quarter of 2020. CPPI’s Taylor BCTMP mill is currently scheduled to complete its maintenance outage in the third quarter of 2020 with a projected 5,000 tonnes of reduced BCTMP production.

Looking forward, CPPI anticipates global softwood pulp demand will remain weak through the third quarter of 2020, against a backdrop of tepid demand for most pulp products, elevated inventory levels and the ongoing weakness in demand for printing and writing paper.

Commenting on the Company’s second quarter results, Canfor’s President and Chief Executive Officer, Don Kayne, said, “We continue to be focused on protecting the health and safety of our employees in the current COVID-19 environment. Having overcome the many challenges faced in the second quarter, it is encouraging to see the current strength of lumber demand and prices and we value the strong relationships we have with our global customers. In addition, the recent acquisition of Elliott and Vida’s announced acquisition of three sawmills from Bergs, continues our strategy of global diversification. While markets appear strong for the third quarter, we remain somewhat cautious about the outlook thereafter, recognizing the inherent uncertainties created by COVID-19. For our pulp business, prices are projected to be challenging through the third quarter; however, as a result of our planned summer fibre-related downtime, we expect our pulp mills to be well placed to run at full capacity through the winter.”

For the full second quarter results, click here.

About Canfor Corporation

Canfor is a leading integrated forest products company based in Vancouver, British Columbia (“BC”) with interests in BC, Alberta, North and South Carolina, Alabama, Georgia, Mississippi and Arkansas, as well as in Sweden with its majority acquisition of Vida Group. Canfor produces primarily softwood lumber and also owns a 54.8% interest in Canfor Pulp Products Inc., which is one of the largest global producers of market Northern Bleached Softwood Kraft Pulp and a leading producer of high performance kraft paper. Canfor shares are traded on The Toronto Stock Exchange under the symbol CFP. For more information visit canfor.com.

Contact:

Pat Elliott – Vice President Corporate Finance & Strategy – Patrick.elliot@canfor.com – (604) 661-5441

Source: Canfor Corporation

The Value of Membership

As the leading provider of in-depth business and credit information on the domestic lumber & forest products industry, a membership with Blue Book Services gives you access to:

- Ratings & Business Reports

- Dynamic Search Tools

- Real-Time Data