Fastenal Company Reports 2021 Annual and Fourth Quarter Earnings

Fastenal Company, a leader in the wholesale distribution of industrial and construction supplies, today announced its financial results for the quarter and year ended December 31, 2021. Except for share and per share information, or as otherwise noted below, dollar amounts are stated in millions. Throughout this document, percentage and dollar calculations, which are based on non-rounded dollar values, may not be able to be recalculated using the dollar values included in this document due to the rounding of those dollar values.

Performance Summary

Year-Over-Year Quarterly Results of Operations

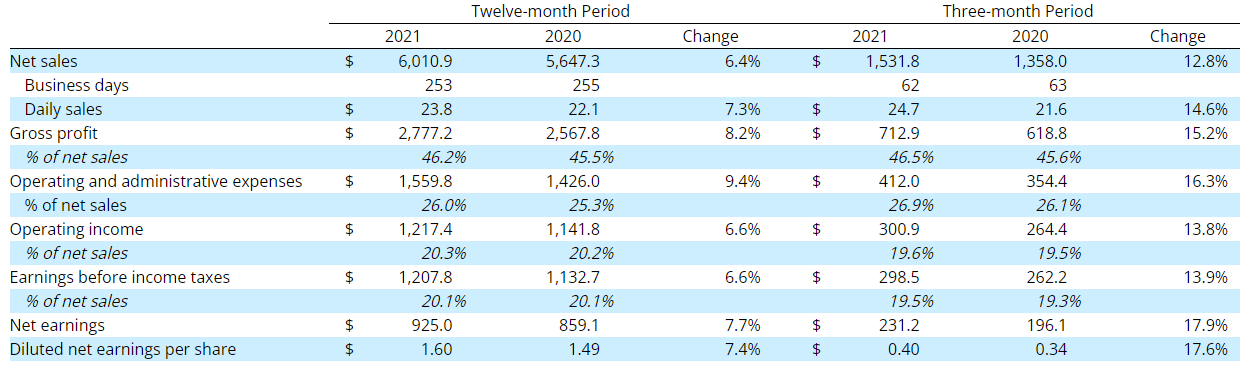

Net sales increased $173.8, or 12.8%, in the fourth quarter of 2021 when compared to the fourth quarter of 2020. There was one fewer selling day in the quarter relative to the year earlier period, and taking this into consideration our net daily sales growth increased 14.6% in the fourth quarter of 2021 when compared to the fourth quarter of 2020. The fourth quarter of 2021 continued to experience strong, economically-driven growth in underlying demand for manufacturing and construction equipment and supplies, which drove higher unit sales that contributed to the increase in net sales in the period. This strength was aided by fewer holiday-related customer facility shut-downs than we typically experience. Similar to the third quarter of 2021, our growth in the fourth quarter of 2021 was slightly limited by slower growth or contraction in sales of certain products to certain end markets related to the COVID-19 pandemic when compared to the fourth quarter of 2020. For instance, daily sales to government and warehousing customers declined 35.7% and 3.5%, respectively. Daily sales of safety supplies returned to growth, rising 3.5%. This relatively modest increase reflects strong growth in vended product to our traditional customer base, partly offset by lower sales for high volume, direct shipments of pandemic-related product that were prevalent in the year earlier period. Daily sales of janitorial products (a subset of other products) decreased 3.4%. The effect of pandemic-related activity on comparisons moderated in the fourth quarter of 2021.

The overall impact of product pricing on net sales in the fourth quarter of 2021 was 440 to 470 basis points. This increase reflects pricing actions taken during 2021, including in the fourth quarter of 2021, as part of our strategy to mitigate the impact of marketplace inflation, particularly for fasteners and transportation services, on our gross margin percentage. Costs remain significantly above year-earlier levels, and we will continue to take actions aimed at mitigating the impact of product and transportation cost inflation as the need arises in 2022. The impact of product pricing on net sales was immaterial during the fourth quarter of 2020.

Pandemic-related effects were still evident when comparing product mix in the fourth quarter of 2021 to the fourth quarter of 2020, though these impacts have moderated versus what was experienced at the height of the pandemic. Fastener daily sales increased 24.2% over the fourth quarter of 2020, and represented 33.5% of our net sales in the fourth quarter of 2021; fasteners represented 30.8% and 33.6% of net sales in the fourth quarter of 2020 and the fourth quarter of 2019, respectively. Improvement in daily sales from the fourth quarter of 2020 reflected higher manufacturing and construction demand, and higher product prices. Safety product daily sales increased 3.5% from the fourth quarter of 2020 and represented 21.4% of our net sales in the fourth quarter of 2021; safety products represented 23.5% and 18.7% of net sales in the fourth quarter of 2020 and the fourth quarter of 2019, respectively. The increase in daily sales reflects strong growth and higher pricing to our traditional manufacturing and construction customers, partly offset by declines of pandemic-related products to certain customers as demand has moderated, supply has broadened, and unit prices on specific products have declined. Other products daily sales increased 12.8% over the fourth quarter of 2020 and represented 45.1% of our net sales in the fourth quarter of 2021; other products represented 45.7% and 47.7% of net sales in the fourth quarter of 2020 and the fourth quarter of 2019, respectively. The increase in daily sales reflects strong growth and higher pricing to our traditional manufacturing and construction customers, slightly offset by declines of pandemic-related products, particularly janitorial and sanitation products.

Daily sales to our national account customers (defined as customer accounts with a multi-site contract) increased 19.9% in the fourth quarter of 2021 over the fourth quarter of 2020. Most of our national account customers grew in the fourth quarter of 2021 over the year earlier period, as reflected by our experiencing growth at 82 of our Top 100 national account customers (and 87 of our Top 100 customers in December 2021). Revenues attributable to national account customers represented 57.8% of our total revenues in the period. Daily sales to our non-national account customers, which includes government customers, increased 7.6% in the fourth quarter of 2021 from the fourth quarter of 2020. Excluding the decline in government daily sales, non-national account daily sales grew at a mid-teens rate reflecting strength in our traditional manufacturing and construction customers due to healthy underlying business conditions. Revenues attributable to non-national account customers represented 42.2% of our total revenues in the period.

Our gross profit, as a percentage of net sales, increased 90 basis points to 46.5% in the fourth quarter of 2021 from 45.6% in the fourth quarter of 2020. This increase reflects a couple of items. First, product margins improved, primarily due to a higher gross profit percentage for our safety products. This was due to both a decline in the mix of lower margin COVID-affected sales and improved margins for those products, as well as a slightly higher margin on non-COVID-affected products. Second, overhead absorption/organizational cost leverage was very strong primarily due to stronger business conditions and sales growth. These positive impacts were only partly offset by higher transportation expenses related to higher overseas shipping costs, port costs, and third-party freight charges. The net impact of product and customer mix was immaterial in the fourth quarter of 2021, as the additive impact of product mix on our gross profit percentage was mostly offset by the dilutive impact of customer mix. The impact of price/cost on our gross profit percentage was similarly immaterial in the fourth quarter of 2021.

Our operating income, as a percentage of net sales, increased slightly to 19.6% in the fourth quarter of 2021 from 19.5% in the fourth quarter of 2020. The increase in our operating income percentage in the fourth quarter of 2021 was due to the 90 basis point increase in our gross profit, as a percentage of net sales, partly offset by an 80 basis point increase in our operating and administrative expenses, as a percentage of net sales, to 26.9% in the fourth quarter of 2021 from 26.1% in the fourth quarter of 2020. The increase in the fourth quarter of 2021 of our operating and administrative expenses, as a percentage of net sales, primarily reflects higher employee-related expenses and higher other operating expenses.

Employee-related expenses, which represent approximately 70% of total operating and administrative expenses, increased 16.5% in the fourth quarter of 2021 compared to the fourth quarter of 2020. We experienced an increase in employee base pay due to higher average FTE during the period, though this grew more slowly than sales, higher wages, and including a greater proportion of full-time employees in our employee pool. We also experienced a significant increase in bonus and commission payments, reflecting improved business activity and financial performance versus the year-ago period, as well as an increase in health insurance costs as employees and their families were more comfortable seeking health care. Occupancy-related expenses, which represent 15% to 20% of total operating and administrative expenses, increased 7.5% in the fourth quarter of 2021 compared to the fourth quarter of 2020. This was primarily due to the timing of development costs related to equipment utilized as part of our Fastenal Managed Inventory (‘FMI’) suite of technologies. Combined, all other operating and administrative expenses, which represent 10% to 15% of total operating and administrative expenses, increased 30.6% in the fourth quarter of 2021 compared to the fourth quarter of 2020. The increase in operating and administrative expenses relates to a 121.4% increase in travel-related costs as activity continues to normalize in contrast to pandemic-related restrictions that presided in the year earlier period, a 108.3% increase in non-healthcare-related insurance costs, a 61.0% increase in fuel costs related to our local truck fleet, and higher spending on business supplies.

Our net interest expense was $2.4 in the fourth quarter of 2021 compared to $2.2 in the fourth quarter of 2020.

We recorded income tax expense of $67.3 in the fourth quarter of 2021, or 22.6% of earnings before income taxes. Income tax expense was $66.1 in the fourth quarter of 2020, or 25.2% of earnings before income taxes. We believe our ongoing tax rate, absent any discrete tax items or broader changes to tax law, will be approximately 24.5%.

Our net earnings during the fourth quarter of 2021 were $231.2, an increase of 17.9% compared to the fourth quarter of 2020. Our diluted net earnings per share were $0.40 during the fourth quarter of 2021, which increased from $0.34 during the fourth quarter of 2020.

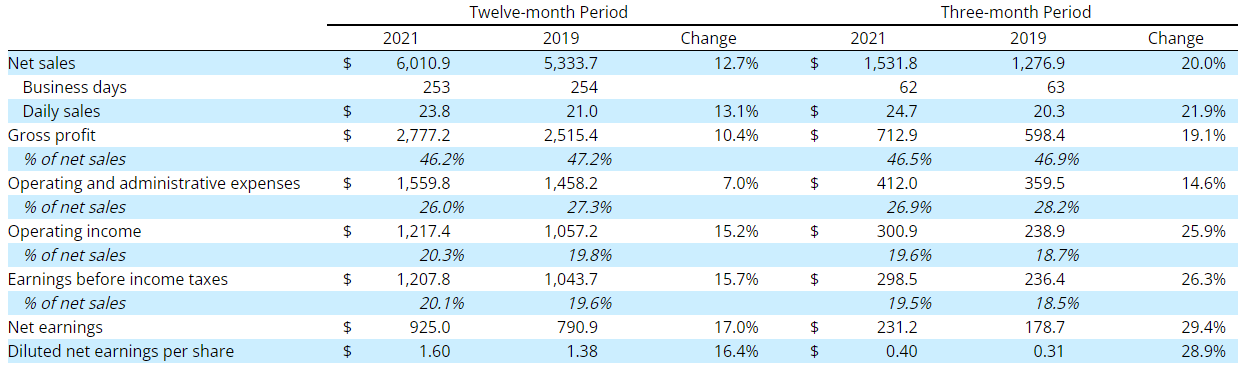

Performance Summary (Comparison to 2019 Periods)

Given the unusual nature of our marketplace during 2021 and 2020 due to the COVID-19 pandemic, we believe that a comparison of certain results of operations during the year and fourth quarter of 2021 to the same periods in 2019 provides further insight into sustainable trends and underlying performance of our business. As discussed earlier in this release, there were certain aspects of the COVID-19 pandemic that dramatically impacted our business during 2020. Given this, we believe that a comparison to the 2019 periods is helpful to demonstrate changes in financial condition and our results of operations during the most recently ended quarter and year. The table below provides such a comparison:

Growth Driver Performance

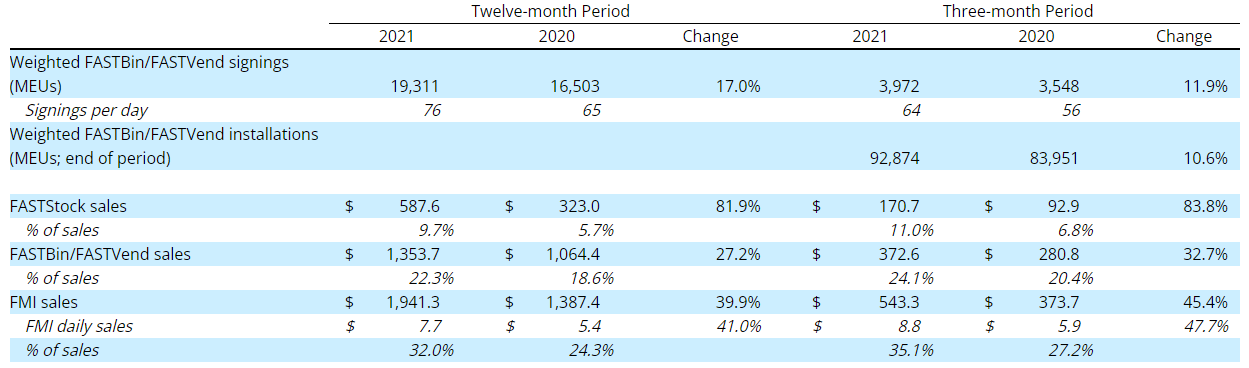

- During 2021, we signed 274 new Onsite locations (defined as dedicated sales and service provided from within, or in close proximity to, the customer’s facility). This included 68 signings in the first quarter of 2021, 87 in the second quarter of 2021, 75 signings in the third quarter of 2021, and 44 signings in the fourth quarter of 2021. We had 1,416 active sites on December 31, 2021, which represented an increase of 11.9% from December 31, 2020. Daily sales through our Onsite locations, excluding sales transferred from branches to new Onsites, grew at a better than 20% rate in the fourth quarter of 2021 over the fourth quarter of 2020. This growth is due to improved business activity from our Onsite customers and, to a lesser degree, contributions from the increase in the number of Onsites we operate. Our Onsite signings in the fourth quarter of 2021 were below our expectations, which we continue to believe is a function of a lengthening of the sales cycle due to the near-term challenges posed by inflation, supply chain constraints, labor shortages, and the pandemic. We continue to believe the market will support a long-term rate of 375 to 400 annual signings, and this represents our goal for Onsite signings in 2022. It is likely that some normalization in the business environment that allows customers to prioritize long-term strategic decision-making over short-term crisis management will be required to achieve this goal.

- FMI Technology is comprised of our FASTStock (scanned stocking locations), FASTBin (infrared, RFID, and scaled bins), and FASTVend (vending devices) offering. FASTStock’s fulfillment processing technology is not embedded, is relatively inexpensive and highly flexible in application, and delivered using our proprietary mobility technology. FASTBin and FASTVend incorporate highly efficient and powerful embedded data tracking and fulfillment processing technologies. Prior to 2021, we reported exclusively on the signings, installations, and sales of FASTVend. Beginning in the first quarter of 2021, and as detailed previously in our 2020 Form 10-K filing, we began disclosing certain statistics around our FMI offering. The first statistic is a weighted FMI measure which combines the signings and installations of FASTBin and FASTVend in a standardized machine equivalent unit (MEU) based on the expected output of each type of device. We do not include FASTStock in this measurement because scanned stocking locations can take many forms, such as bins, shelves, cabinets, pallets, etc., that cannot be converted into a standardized MEU. The second statistic is revenue through FMI Technology which combines the net sales through FASTStock, FASTBin, and FASTVend. A portion of the growth in net sales experienced by FMI, particularly FASTStock and FASTBin, reflects the migration of products from less efficient non-digital stocking locations to more efficient, digital stocking locations. Figures reported prior to 2021 may differ slightly from those provided in our 2020 Form 10-K filing based on minor changes we made to the conversion of absolute devices to weighted devices.

The table below summarizes the signings and installations of, and sales through, our FMI devices.

Our FMI signings in the fourth quarter and 2021 trended below expectations. Similar to Onsites, we believe seasonality and the near-term challenges posed by inflation, supply chain constraints, labor shortages, and the pandemic are lengthening the selling cycle. Our goal for weighted FASTBin and FASTVend device signings in 2022 is 23,000 to 25,000 MEUs.

All metrics provided above exclude approximately 12,000 non-weighted vending devices that are part of a leased locker program.

- Our eCommerce business includes sales made through an electronic data interface (EDI), or other types of technical integrations, and through our web verticals. Daily sales through eCommerce grew 45.2% in 2021 and grew 48.2% in the fourth quarter of 2021. Revenues attributable to eCommerce represented 15.0% of our total revenues in the fourth quarter of 2021.

Our digital products and services are comprised of sales through FMI (FASTStock, FASTBin, and FASTVend) plus that proportion of our eCommerce sales that do not represent billings of FMI services (collectively, our Digital Footprint). We believe the data that is created through our digital capabilities enhances product visibility, traceability, and control that reduces risk in operations and creates ordering and fulfillment efficiencies for both ourselves and our customers. As a result, we believe our opportunity to grow our business will be enhanced through the continued development and expansion of our digital capabilities.

Our Digital Footprint in the fourth quarter of 2021 represented 46.4% of our sales. We began to provide this figure in the first quarter of 2021, when we reported that our Digital Footprint represented 34.8% of our sales. We subsequently identified a calculation error. Using the same approach to calculating our Digital Footprint as we used in the second, third, and fourth quarters of 2021, our Digital Footprint represented 39.1% of our sales in the first quarter of 2021.

Balance Sheet and Cash Flow

We produced operating cash flow of $770.1 in 2021, a decrease of 30.1% from 2020, representing 83.3% of the period’s net earnings versus 128.3% in 2020. The decline in our operating cash flow and conversion rate is primarily due to an increased need for working capital to support our customer’s growth as business activity improves, as well as from inflation in inventory. Customer mix also contributes in two ways. First, our mix of traditional manufacturing and construction customers normalized along with general business conditions and were a greater proportion of our sales mix in 2021 than was the case in 2020; these customers tend to have longer payment terms and retain more inventory on hand. Second, national accounts continue to grow in our sales mix, and these customers tend to have longer payment terms. These impacts were only partly offset by growth in profits.

Accounts receivable were $900.2 at the end of 2021, an increase of $130.8, or 17.0%, over the end of 2020. Our accounts receivable balance increased due to several factors. First, our receivables are expanding as a result of improved business activity and resulting growth in our customers’ sales. Second, in response to the COVID-19 pandemic, customers that traditionally have shorter payment terms represented a smaller proportion of our sales mix at the end of 2021 than was the case at the end of 2020. Inventory was $1,523.6 at the end of 2021, an increase of $186.1, or 13.9%, over the end of 2020. This reflects significant inflation in the value of stocked parts. It also reflects the addition of inventory to support the growth of our manufacturing and construction customers as they expand production to meet improved business activity and deeper inventory stocking due to disruptions in supply chains. Accounts payable were $233.1 at the end of 2021, an increase of $26.1, or 12.6%, over the end of 2020 due to our product purchases increasing to support the improvement in business activity at our manufacturing and construction customers.

Our investment in property and equipment, net of proceeds from sales, was $148.2 in 2021 compared to $157.5 in 2020. We had higher spending on an office building construction project in Winona, Minnesota intended to support growth in our business. This was more than offset by reduced spending in other areas. We saw a significant decline in spending on FMI equipment due to slower hardware signings, lower vending equipment costs following the March 2020 acquisition of certain industrial vending assets of Apex Industrial Technologies LLC, and an increase in the refurbishment and redeployment of FMI hardware as an alternative to buying new devices. We also had lower capital investment in our hub properties following a period of heavier investment in 2018 and 2019, and reduced spending on selling-related vehicles as challenges in the supply chain reduced availability. We expect our investment in property and equipment, net of proceeds of sales, in 2022 to be $180.0 to $200.0. This reflects an increase in spending on FMI equipment in anticipation of higher signings, an increase in spending on hub properties to reflect upgrades to and investments in automation as well as facilities upgrades, and an increase in manufacturing capacity to support demand and expand capabilities. This is partly offset by the absence of spending on our Winona construction project, which was completed in 2021.

We returned $643.7 to our shareholders in 2021 in the form of dividends, compared to $855.4 in 2020 in the form of dividends ($803.4) and purchases of our common stock ($52.0). Our 2020 dividends included a special supplemental dividend of $229.6 ($0.40 per share) which was a result of our high cash balances and favorable financial outlook.

Total debt on our balance sheet was $390.0 at the end of 2021, or 11.4% of total capital (the sum of stockholders’ equity and total debt). This compares to $405.0, or 12.9% of total capital, at the end of 2020.

Additional Information

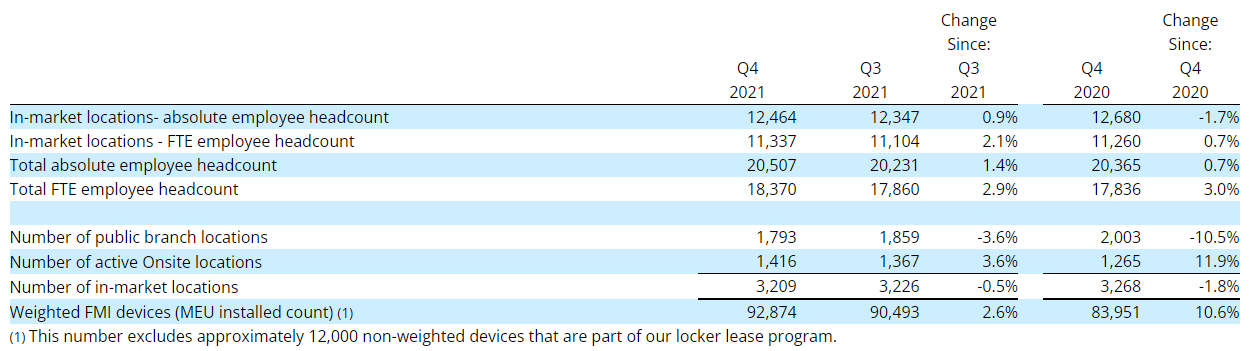

The table below summarizes our total and FTE (based on 40 hours per week) employee headcount, our investments related to in-market locations (defined as the sum of the total number of public branch locations and the total number of active Onsite locations), and weighted FMI devices at the end of the periods presented and the percentage change compared to the end of the prior periods.

During the last twelve months, we increased our total FTE employee headcount by 534. This reflects an increase in our in-market and non-in-market selling FTE employee headcount of 230 to support growth in the marketplace and sales initiatives targeting customer acquisition. We had an increase in our distribution center FTE employee headcount of 149 to support increasing product throughput at our facilities and to expand our local inventory fulfillment terminals (LIFTs). We had an increase in our remaining FTE employee headcount of 155 that relates primarily to personnel investments in information technology and operational support, such as purchasing and product development.

We opened two branches in the fourth quarter of 2021 and closed 68 branches, net of conversions. We activated 65 Onsite locations in the fourth quarter of 2021 and closed 16, net of conversions. In 2021, we opened ten branches and closed 220, net of conversions. In 2021, we activated 242 Onsite locations and closed 91, net of conversions. In any period, the number of closings tend to reflect both normal churn in our business, whether due to redefining or exiting customer relationships, the shutting or relocation of customer facilities that host our locations, or a customer decision, as well as our ongoing review of underperforming locations. Our in-market network forms the foundation of our business strategy, and we will continue to open or close locations as is deemed necessary to sustain and improve our network, support our growth drivers, and manage our operating expenses.

For the complete press release, click here.

Contact:

Ellen Stolts – Director of Accounting, Reporting & Reconciliation – (507) 313-7282

Source: Fastenal Company

The Value of Membership

As the leading provider of in-depth business and credit information on the domestic lumber & forest products industry, a membership with Blue Book Services gives you access to:

- Ratings & Business Reports

- Dynamic Search Tools

- Real-Time Data