Barchart: Lumber Zzzzzz

The lumber futures market has gone to sleep. Random-length lumber futures for nearby delivery have been trading between $400 and $567 per 1,000 board feet since September. While the winter is the offseason for construction demand, rising US interest rates have weighed on new home purchases, translating to lower lumber requirements.

The lumber market has gone to sleep in late 2022, and the prospects for even high interest rates in 2023 are a bearish factor for wood prices. However, illiquidity in the lumber futures arena can cause extreme price volatility. As the market moves towards 2023 and the spring, we could see a recovery in the market that tends to be a barometer for other industrial commodity prices.

Lumber has remained above the $400 level

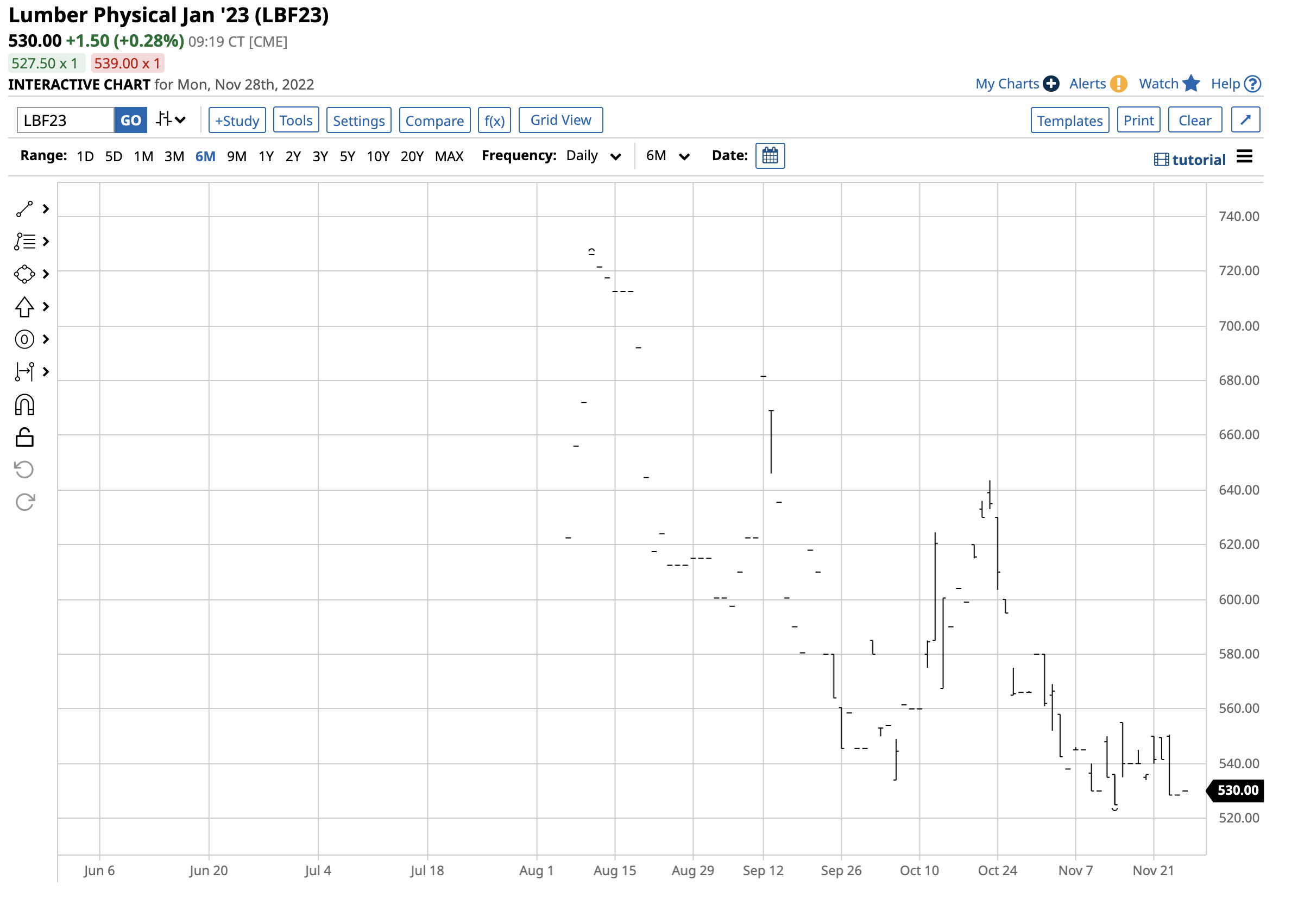

Nearby lumber futures have gone to sleep since early November.

The chart highlights that random-length lumber futures for January delivery have traded between $411.10 and $453.20 per 1,000 board feet since November 3. The $42.10 range has been a coma-like environment for the lumber market, which traded at $1711.20 on May 2021 and $1477.40 in March 2022. The wild price swings have given way to a narrow price band. At the $425 level on November 28, lumber futures remain directionless near the low.

The trend remains bearish for three reasons

Since reaching a record high in May 2021 and making a lower peak in March 2022, lumber futures have been in a bear market. Three factors continue to weigh on wood’s price at the $425 level on November 28:

- Rising US interest rates have pushed conventional thirty-year fixed-rate US mortgages from below 3% in late 2021 to over 7% in November 2022. The increase in financing has caused the number of new home buyers without cash to evaporate, weighing on lumber demand for new home construction.

- Aside from higher interest and mortgage rates, the rapid rise of home prices over the past years has priced out many potential buyers, further decreasing lumber demand.

- Supply chain bottlenecks during the pandemic have eased, allowing for the flow of wood, and decreasing the supply issues that faced the lumber market in 2020 and 2021.

The bottom line is that lumber had risen to unsustainable levels over the past years. While lumber futures declined to the $425 level, we must remember that before 2018, the record high was at $493.50, the 1993 peak.

The new physical lumber contract remains at a significant premium to the random-length contract

The CME rolled out a new physical lumber futures contract to attract more hedging and other market activity. The physical contract is smaller, 27,500 board feet versus 110,000 board feet. It included more lumber grades and could accommodate truck instead of railcar loads. While the January random-length lumber contract was at the $425 level on November 28, the physical contract was trading at a far higher price.

The chart illustrates the January physical lumber contract at $530 was at a $105 premium to the random-length lumber contract for the same delivery.

A barometer for other raw material prices

With over forty years of experience in the commodity markets, there are few raw material futures that I have not traded. Since 1981, I have ventured into even the most obscure markets but have never traded one lumber contract. Liquidity is a crucial factor for hedgers, traders, and investors. The ability to get into a risk position and exit on a reasonable bid-offer spread is a primary consideration for anyone considering participation. Unfortunately, lumber has been what many traders call a “roach motel.” Entering a long or short position is possible when the price moves against the anticipated direction. Exiting is plausible when selling during a rally or buying during a dip. However, selling when the price is falling or buying when it is rising can cause execution slippage that destroys the economics of the trade or investment.

While I have never traded lumber, I watch the price like a hawk, considering wood’s price level and path of least resistance as important as other industrial commodities, including oil, copper, steel, and others. Lumber is a critical infrastructure building block, and its illiquidity often leads the lumber futures arena to experience dramatic moves that provide clues for other, more liquid markets. I view lumber as a barometer that takes the overall temperature of the industrial commodities sector. In November 2022, the price is sitting near the recent low, but we are also in the offseason for construction during a highly uncertain time in markets across all asset classes. Lumber’s slumber is a commentary on the overall state of markets across all asset classes in late 2022.

A pivot from the Fed could ignite another explosive lumber rally

The US Federal Reserve likely holds the key to the path of least resistance of the lumber market. The central bank has committed to fighting inflation via a hawkish monetary policy path. The latest consumer and producer price index data indicates inflation may have peaked and be heading lower. If the Fed backs off, we could see a sudden surge in stocks, bonds, and commodity prices, including lumber. Lower interest rates will take the pressure off mortgage rates, increasing the demand for wood.

Moreover, lumber’s illiquidity could cause the wood price to move dramatically before other markets and provide a signal for other commodities and asset classes.

Meanwhile, the physical contract has yet to attract the volume and open interest levels that CME had hoped, but it is early days. Time will tell if the premium for physical lumber over the random-length contract is a clue that the Fed is closer to a dovish pivot than the overall market believes.

To view the original post, click here.

Article Author: Andrew Hecht

Source: Barchart.com, Inc.

The Value of Membership

As the leading provider of in-depth business and credit information on the domestic lumber & forest products industry, a membership with Blue Book Services gives you access to:

- Ratings & Business Reports

- Dynamic Search Tools

- Real-Time Data