HNI Corporation Reports Earnings for First Quarter Fiscal Year 2023

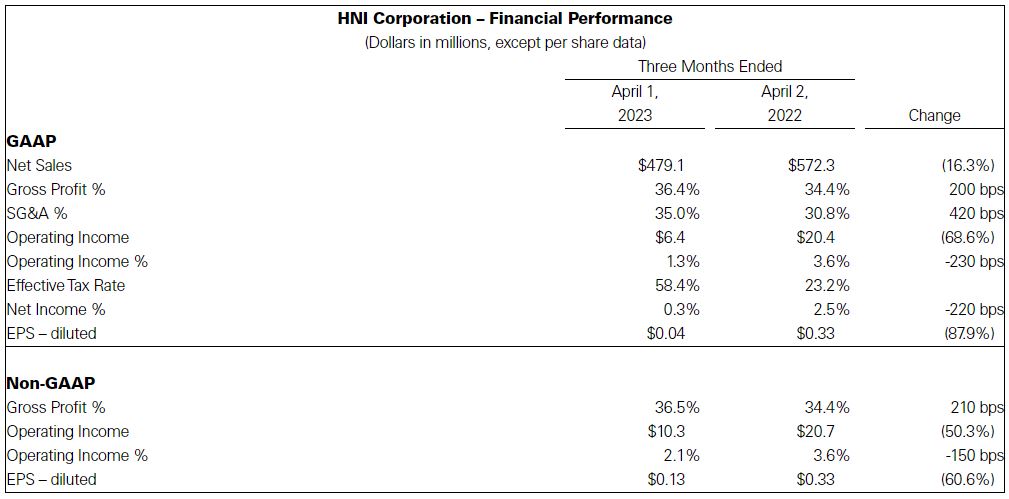

HNI Corporation (the “Corporation”) announced sales for the first quarter ended April 1, 2023 of $479.1 million and net income of $1.6 million. GAAP net income per diluted share was $0.04, compared to $0.33 in the prior year. Non-GAAP net income per diluted share was $0.13, compared to $0.33 in the prior year. GAAP to non-GAAP reconciliations follow the financial statements in this release.

First Quarter Highlights

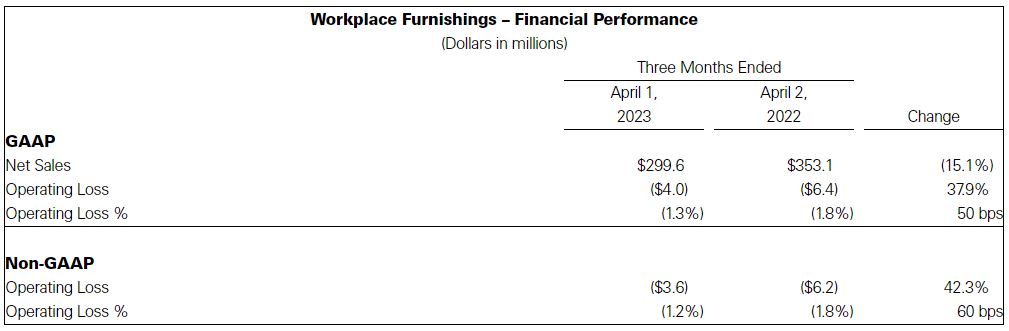

- Profit growth actions in Workplace Furnishings delivering results – A return of annual net productivity savings, benefits from streamlining efforts and cost actions implemented in 2022, and continued improvement of price-cost provided profitability support in the first quarter. As a result, the first quarter seasonal non-GAAP operating loss in Workplace Furnishings narrowed by more than 40 percent on a year-over-year basis, despite top line pressure associated with prior-year backlog dynamics and weaker macroeconomic conditions. The first quarter marked the fourth consecutive quarter of year-over-year profit improvement in Workplace Furnishings.

- Demand in Workplace Furnishings supports long-term optimism, although near-term conditions remain dynamic – Workplace Furnishings revenue in the first quarter surpassed the Corporation’s previous outlook with shipments to small-to-medium sized businesses and to contract customers both exceeding expectations. Organic orders grew 13 percent in the first quarter compared to the prior year reflecting improving demand trends, the Corporation’s unique market position, and the benefit of pull-forward activity driven by price increases.

- Update on Kimball International deal – On March 8, 2023, the Corporation announced an agreement to acquire Kimball International (NASDAQ: KBAL; “Kimball”) in a cash and stock transaction currently valued at approximately $455 million. The transaction has cleared antitrust review with the statutory waiting period under the Hart-Scott-Rodino Antitrust Improvements Act expiring on April 20, 2023. The Corporation expects the transaction to close in early June following i) satisfaction of customary closing conditions and ii) approval by the Kimball shareholders at the special shareholder meeting set for May 31, 2023. The combination creates a market leader that is strongly positioned for post-pandemic trends with an expanded presence in secondary geographies and expertise in ancillary products. The combined company is expected to have pro forma annual revenue of approximately $3 billion and pro forma adjusted EBITDA of approximately $305 million, inclusive of an estimated $25 million in annual run-rate synergies.

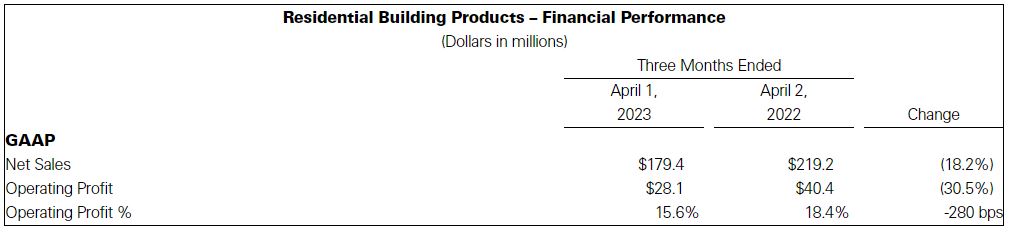

- Residential Building Products prepared for lower demand – Consistent with the Corporation’s previously discussed expectations, higher interest rates and economic uncertainty negatively impacted Residential Building Products segment demand in the first quarter. However, productivity savings, cost reduction actions, and continued price-cost improvement offset nearly half of the volume-related profit pressure. As a result, segment operating margin remained in the mid-teens.

“Our actions to drive profit expansion in Workplace Furnishings are delivering results, as reflected in our better-than-expected first quarter profitability. Demand trends in Workplace Furnishings are also encouraging with higher-than-anticipated order growth across our businesses. Our Residential Building Products segment performed largely as expected as we adjusted to softer housing-related demand conditions and held operating margins above 15 percent for the 11th straight quarter,” stated Jeff Lorenger, Chairman, President, and Chief Executive Officer.

First Quarter Summary Comments

- Consolidated net sales decreased 16.3 percent from the prior-year quarter to $479.1 million. On an organic basis, sales decreased 14.0 percent year-over-year. The sale of the Corporation’s China- and Hong Kong-based Lamex office furniture business (“Lamex”) in the third quarter of 2022 decreased year-over-year sales $17.2 million, while the acquisition of a residential building products company in the second quarter of 2022 increased year-over-year sales by $1.5 million. A reconciliation of organic sales, a non-GAAP measure, follows the financial statements in this release.

- Gross profit margin expanded 200 basis points compared to the prior-year quarter. This increase was driven by favorable price-cost and improved net productivity, partially offset by lower volume.

- Selling and administrative expenses as a percent of sales increased 420 basis points compared to the prior-year quarter. The increase was driven by one-time costs associated with the planned acquisition of Kimball, lower volume, higher freight expense, and increased investment spend. These factors were partially offset by price realization and lower core SG&A.

- Non-GAAP net income per diluted share was $0.13 compared to $0.33 in the prior-year quarter. The decrease was primarily driven by lower volume, which was partially offset by favorable price-cost, lower core SG&A, and improved net productivity.

- Non-GAAP net income per diluted share in the current quarter includes an effective tax rate of 30.5 percent, compared to a GAAP tax rate of 58.4 percent. The higher GAAP rate was driven by non-deductible costs related to the planned acquisition of Kimball.

- Workplace Furnishings net sales decreased 15.1 percent from the prior-year quarter to $299.6 million. On an organic basis, sales decreased 10.8 percent year-over-year. The impact of the sale of Lamex in the third quarter of 2022 decreased sales $17.2 million compared to the prior-year quarter.

- Workplace Furnishings GAAP operating margin improved 50 basis points versus the prior-year quarter, driven by favorable price-cost, lower core SG&A, and improved net productivity, partially offset by lower volume.

- Residential Building Products net sales decreased 18.2 percent from the prior-year quarter to $179.4 million. On an organic basis, sales decreased 18.8 percent year-over-year. The impact of a residential building products company acquired in the second quarter of 2022 increased sales $1.5 million compared to the prior-year quarter.

- Residential Building Products operating profit margin compressed 280 basis points year-over-year, driven by lower volume, partially offset by favorable price-cost.

First Quarter Orders

- Organic orders in the Workplace Furnishings segment increased 13 percent versus the same period a year ago. This rate benefited from pull-forward activity associated with price increases that became effective during the quarter. Orders from small-to-medium sized customers and orders from larger contract customers increased at a similar rate.

- Orders in the Residential Building Products segment decreased 37 percent compared to the prior-year period, versus a positive 27 percent year-ago comparable. Orders in the remodel/retrofit channel were weaker than those in the new construction market during the quarter.

Fiscal Year 2023 Outlook

- Demand environment – The Corporation expects weaker macroeconomic conditions to continue to impact Workplace Furnishings demand and profitability on a year-over-year basis through the second quarter. In Residential Building Products, the Corporation expects a weak housing market to result in year-over-year revenue and profit pressure persisting through the remainder of 2023. However, the rate of decline is expected to moderate in the second half primarily due to a return to normal seasonality and less challenging year-ago comparables.

- Seasonality expectations – The Corporation continues to expect earnings seasonality will be more in-line with pre-pandemic trends. This follows three years of abnormal seasonal trends with 2022 seasonality being particularly impacted by backlog dynamics and deteriorating demand. The difference in seasonality between 2023 and 2022 will distort quarterly year-over-year comparisons of sales and profit in 2023. The Corporation now expects to generate approximately 80 percent of its annual profit in the second half of 2023, compared to approximately 60 percent in the second half of 2022.

- Second quarter commentary – The Corporation expects second quarter 2023 operating income to exceed first quarter 2023 levels. The sequential profit increase assumes seasonal revenue growth and continued benefits from profit improvement actions in Workplace Furnishings. This will be partially offset by lower profit in Residential Building Products, which is expected to be negatively impacted by continued housing-related pressures and the return of normal seasonality. The second quarter outlook excludes any impact from closing the Kimball transaction.

Concluding Remarks

“We are well positioned for both the current environment and the long-term. In Workplace Furnishings, our profit improvement actions will continue to drive results. Our combination with Kimball International will create a market leader uniquely positioned for the post pandemic environment with expertise in both secondary geographies and ancillary products. These capabilities and market positions are becoming increasingly important due to population migration and hybrid work trends.

“In Residential Building Products, while we are prepared for weak near-term demand, we remain focused on driving long-term growth. We continue to have unique opportunities to grow our business through driving category awareness, leading product innovation, and expanding our owned installing-distribution footprint. The mid- and long-term fundamentals of the housing market are strong. The market is undersupplied, and demographic trends support demand growth.

“We remain committed to our core strategies, which will expand margins in Workplace Furnishings and drive long-term revenue growth in Residential Building Products,” Mr. Lorenger concluded.

For the full first quarter results, click here.

About HNI Corporation

HNI Corporation (NYSE: HNI) is a manufacturer of workplace furnishings and residential building products, operating under two segments. The Workplace Furnishings segment is a leading global designer and provider of commercial furnishings, going to market under multiple unique brands. The Residential Building Products segment is the nation’s leading manufacturer and marketer of hearth products, which include a full array of gas, electric, wood, and pellet-burning fireplaces, inserts, stoves, facings, and accessories. More information can be found on the Corporation’s website at www.hnicorp.com.

Contact:

Marshall H. Bridges – Senior Vice President and Chief Financial Officer – (563) 272-7400

Source: HNI Corporation

The Value of Membership

As the leading provider of in-depth business and credit information on the domestic lumber & forest products industry, a membership with Blue Book Services gives you access to:

- Ratings & Business Reports

- Dynamic Search Tools

- Real-Time Data